![]() I’ve nearly recovered from the payments overload that was Money2020 last week in Las Vegas – it was initially exhilarating, then incredibly exhausting, but I had a fantastic time. Here’s my admittedly subjective take based on having attended only two sessions (one of which I moderated) and stood in the back for only part of a couple more, but having had dozens of formal and informal briefings, taken part in many animated hallway conversations, and listening to approximately half of the Money2020 keynotes.

I’ve nearly recovered from the payments overload that was Money2020 last week in Las Vegas – it was initially exhilarating, then incredibly exhausting, but I had a fantastic time. Here’s my admittedly subjective take based on having attended only two sessions (one of which I moderated) and stood in the back for only part of a couple more, but having had dozens of formal and informal briefings, taken part in many animated hallway conversations, and listening to approximately half of the Money2020 keynotes.

First, my accolades to Anil, Jonathan and the whole team at Money2020. In two short years, they have created the must-attend event in payments, with senior level participation, astoundingly good networking (nearly every Glenbrook client in one place), and a chance to catch-up with all my favorite payment geeks. Thank you!

Key themes at Money2020

Interoperability vs. Network Fantasies

Payments has long been a hotbed of network fantasies (mostly unrealized) but we’re starting to see more and more acknowledgment that interoperability rather than comprehensive solutions is paramount to succeeding in the future of payments. The need to seamlessly knit payments into the broader context of shopping requires providers of payments rails to expand beyond the traditional open loop model (banks representing payers and payees, with a payment network in the middle). Banks and the card networks are fast-tracking their efforts to experiment with loyalty and offers. Meanwhile, the non-traditional players are forging interconnectivity with POS solutions, we’re starting to see better connectivity between accounting platforms and payment providers (although there is a very long way to go on this front), and even cooperation between the networks themselves (on tokenization).

Rise of non-bank providers

The over-arching narrative of the keynotes on the main stage was the competing efforts of the incumbents (the card networks and their bank customers) and new entrants (Google, PayPal, ISIS, MCX, Amazon, Square, etc.) to be the most relevant to the future of payments.

Some of the new entrants stumbled (ISIS in particular) and the audience was very frustrated that MCX didn’t reveal more in their keynote. Personally, I’ve been advising our clients to pay attention to MCX. The emboldened merchants have more consumer relationships (700 million customer loyalty and payment accounts) than Apple (575 million), PayPal (135 million) and Amazon (215 million) and, were MCX to emulate the Target RED Card with a decoupled debit model, they’d delight the broad swath of Americans that prefer to fund their day to day transactions with debit/current account funds rather than incurring credit.

Meanwhile, bank presence onstage and off was relatively minimal (other than investment bankers running about eagerly seeking the hottest new thing).

Wallet Wars

The mobile payment wallet wars continue, and to be perfectly honest I’m rather tired of it all. Google demonstrated their latest effort, PayPal continues to hone in on offline payments, while Square is moving from offline to online. There are plenty of other commentaries out on mobile at Money2020 so all I am going to say on the matter is that so far – despite really trying – I still pay for all of my transactions at the point of sale with a dumb mag-stripe card. Perhaps iBeacon (e.g. Estimote) and PayPal Beacon will deliver the elusive consumer value prop that will ease us away from our beloved cards. Or perhaps not. [Editors note 10/19/2013: Glenbrook’s Russ Jones has insightful commentary on the mobile wallet wars here.]

Financial Inclusion

The payments universe is paying more attention to non-traditional customers – in particular the un-under-and-unhappily banked. I thought that one of the best keynotes was Dan Schulman from American Express on the network’s efforts to increase financial inclusion (video). Bluebird is the prepaid/bank account alternative product AmEx issues in partnership with Wal-Mart. But Bluebird is really just the tip of the iceberg. The Serve wallet product itself is being re-launched to match the Bluebird offering and AmEx is preparing to expand not just in the US but globally – working with retailers and MNOs – to provide an alternative to traditional checking and debit. Obviously this is key to expanding the reach of the AmEx brand to a very large segment of new underserved customers, but also makes AmEx a more attractive option for everyday merchants who might not have been motivated to accept AmEx previously.

Rethinking Traditional Payment Paradigms

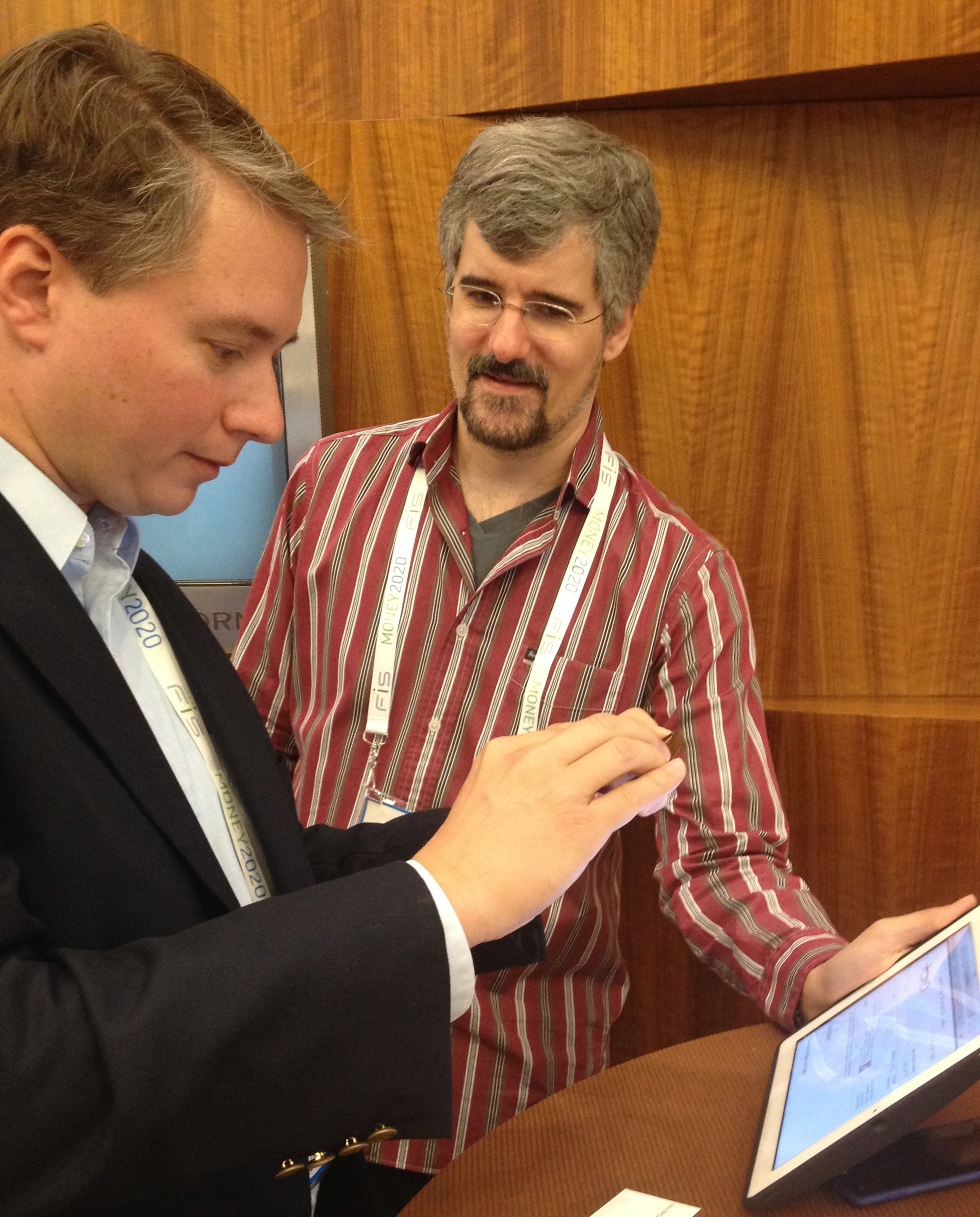

One of the most remarkable demos I had at Money2020 was from VerifyValid‘s Dean Tribble. The company has partnered with Deluxe to enable small businesses to create native digital checks (literally a PDF that resembles a traditional check) that can be emailed to the recipient. Upon receipt, the payee can print it out and take it to a branch or – even easier – take a picture of it with their phone and remotely deposit it. Here’s City National Bank’s Nate Wehunt attempting to take a picture of the check image on screen and deposit it via his mobile banking app:

It didn’t work (the iPad screen glare was too strong) but I heard from Abacus’ Omar Qari that he was able to successfully do a remote deposit using a picture he took from his laptop screen.

Back in the late 90s when I was working on the first image check processing applications (a long way before Check 21) I never imagined such a thing. It’s mind-boggling that we have resorted to workarounds like this to move business payments from paper to electronic.

Uncomfortable Partnerships between Incumbents and New Entrants

One of the most interesting perspectives I heard at Money2020 was from Google’s Carol Grunberg. She spoke at a W.net event on Sunday evening, offering insight to payment incumbents on how to better understand new entrants from outside the industry. She described what Google refers to as the “toothbrush test” – that engineers and product teams are focused on solutions to high frequency (2x a day, hence “toothbrush”) opportunities to add value. Big audacious product and projects that offer benefits and solve a problem for users that they may not even realize they have. Carol remarked that upon starting at Google, she was astonished that in meetings, when starting a project, the economics are never discussed. She was accustomed to doing market sizing exercises, developing budgets, etc. Instead, efforts at Google (and at other tech companies) are engineering led. Economics are secondary “No one talks about how much money we’re going to make, how much will it cost…”

At Google it is expected that there will be many twists and turns along the way (as evidenced by the many permutations of Google Wallet) – the teams are accustomed to iterating and tweaking in order to test how does this benefit the merchant, how does this benefit the consumer? The engineers build something, test it, pilot it, launch it. And continue to iterate, post-launch. “The market will tell us where to go.”

Carol acknowledged that this is very hard for Google’s partners (not just those in the payments industry) who have to know what the game plan is in order to muster resources, that need to have an explicit business plan to gain traction internally, and are facing pressure to deliver quarterly earnings. The Google approach is not only hard for traditional payments players to understand, but likely impossible for them to wait out.

Distributed Models

Whether new approaches to small business loans (Kabbage, OnDeck Capital Access Network, and even Amazon), relying on actual transaction data rather than reviews for restaurants and services (Wisely), or the emergence of state-less currencies (Bitcoin, Ripple) distributed approaches are gaining traction. These new methods up-end the traditional models and are highly dependent on technology and data. They are the future of commerce, not just payments.

B2B Payments

There was precious little business payment coverage at Money2020, but I did moderate a panel with Bill.com’s Rene Lacerte, Billtrust’s Flint Lane and Zipmark’s Jay Bhattacharya. We discussed the stubborn appeal of checks, the need to offer value to both business buyers and suppliers, the relative appeal of ACH and cards, as well as emerging options like Zipmark, and each of the panelists readily admitted to suffering from network fantasies.

Everything you need to know about B2B payments at #money2020 is right here @FlintLane @rlacerte pic.twitter.com/wjbVObugbu

— Erin McCune (@erinmccune) October 8, 2013

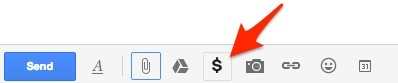

P2P = Game Over

The efforts to attract consumer attention via P2P transfers may be all but over once the ability to attach money to Gmail becomes a reality for the Google customer base (see picture):

Bitcoin (and other virtual currencies) – Froth or Not?

There was intense curiosity about Bitcoin at Money2020, as Mike Laven remarked on stage: “There’s never a session where the b word [Bitcoin] doesn’t come up.” Much more from Glenbrook on Bitcoin here.

My client commitment on the final day of the conference was postponed, so at the last minute I changed my plans and stayed in Las Vegas for the Ripple developer event on Thursday morning. I was impressed. Think of Ripple and Ripple Labs as the next step in the evolution of virtual currencies, making Bitcoin much more readily accessible and helping developers to monetize access not only to Bitcoin but to cross-border transactions in any currency. Virtual currencies are not going away. Admittedly, we are at the very early stages and both the new players and the relevant regulators have a lot of adapting to do. But there is no doubt that math based currencies are here to stay and are potentially very disruptive (particularly for cross-border transactions).

Cool Companies

A very subjective, short list of companies that I though were cool

- Wisely: http://wise.ly/blog/why-did-we-create-wisely

- Subledger: http://subledger.com/

- Jingit: https://www.jingit.com/home/

- Abacus: https://www.abacus.com/

Best Money2020 Quotes

- Matt Harris, Bain Capital: “@Money2020 is the Hunger Games of payments” @mattcharris

- Best Sarah Friar @Square keynote line: “If you are talking to your customer about payments, something has gone wrong” #money2020 @Square @thefriley

- @Payoneer’s Scott Galit: “Technology is enabling us to embed international payments into business processes” #Money2020

- Don Kingsborough, PayPal: “You have to be where the consumer already loves to shop” not a couple merchants, a couple cities #PayPal #money2020

- Dan Schulman, AmEx: “There are more than 2 billion people in the world, and 70 million in the US, that are poorly served by the traditional financial system.”

- Stripe: A “direct assault on payments is a bit like a land war in Asia, you just don’t want to go there” @patrickc #money2020

- And in response: @BitcoinMoney said “We go there”

- On the MCX panel, Kate Jaspon of Dunkin Brands: MCX represents “a lot of competitors working together, doing together what none of us would do alone” #Money2020

- Via Tom Noyes: A retailer said it best “Visa and MasterCard DO things to me.. they never talk to me.. they direct me.. the never listen.. they mandate… “

- @FlintLane: Favorite line from @money2020 – “We all have our network fantasies, let me tell you about ours” B2B Panel w/ @rlacerte @erinmccune @jayastu

Money2020 Soundtrack

How many conference organizers commission their own soundtrack? Here is the sound of Money2020:

- Young Mothers Alliance: Titans of Industry

- The Ehs: A time for Growth

- Divine: New Horizon

A Payments Wager

And finally, a payments wager. This summer, like many sailors, I was caught up in the American’s Cup hosted in San Francisco. I was down at the waterfront on the day that we all presumed Larry Ellison’s Oracle USA team would lose the cup to New Zealand. But Oracle won that race, prompting me to remark to my salty friends, I should place a bet on Oracle coming back from behind and retaining the cup against steep odds. I didn’t place that bet, much to my regret.

In Vegas this last week, I had the same sensation, my instincts prompting a nagging desire to place another bet – this one on the Federal Reserve. I doubt the bookmakers in Vegas accept wagers on the Fed, but if I could, I’d bet that the US financial services community will face a mandate for real-time, good funds push payments within the next five years. The odds are about the same as Team Oracle USA’s historic turn-around, but this time I’m doing it. Want to wager against me?

During her time at Glenbrook, Erin focused on client engagements in business payments, cross-border transactions, bill payment, and the intersection of corporate finance, banking, and ERP/accounting. She has nearly twenty years of experience leading increasingly complex payment initiatives for corporate clients and advising financial institutions and payment technologists on the development of their payment capabilities.

Erin is also the founder of Forte Financial, a consulting firm focused on corporate finance efficiency, technology, and process improvement. She is a past president of the Financial Women’s Association of San Francisco and also a two-term past president of the San Francisco Treasury Management Association. Erin is no longer with Glenbrook, but contributed greatly during her time at the firm.