Economies, global and domestic, are both interconnected and interdependent. Routine perturbations like economic slowdowns and recessions illuminate those dependencies as pain in one sector spreads to an adjacent one.

COVID-19, and the global economic, social, and political reaction to it, put these linkages in high relief.

The COVID-19 pandemic’s disruptive impact on global trade, national economies, and personal consumption, and savings will continue through 2021 with recovery highly dependent upon the development and distribution of effective vaccines and herd immunity.

As individuals and countries, we have a long wait ahead that will demand ongoing adaptations in how we work, educate, buy and sell.

These realities will continue to shape the growth and form of payments activity.

Interconnected Disruptions in Payments

We can illustrate the payments impact by reviewing how a given transaction is dependent upon in-person interactions. In decreasing order of riskiness, a top 10 list provides a useful map of pandemic-affected payment segments.

- Healthcare and social assistance

- Public administration

- Accommodation and food services

- Arts, entertainment, and recreation

- Retail trade

- Other services (except public administration)

- Educational services

- Real estate, rental, and leasing

- Construction

- Utilities

Most of this list is composed of services-sector industries, many of which continue to be affected by the pandemic. A few examples:

Healthcare. Despite the need for healthcare services to address the pandemic itself, the business of healthcare has been hurt by the loss of high margin electives and other profit-making procedures. As a result, healthcare professional services firms have seen a 48% drop in revenue as patients postpone procedures and avoid hospitals and clinics. (Rumor has it that plastic surgery patients have taken advantage of the privacy work-from-home confers. Just keep the video off.)

Tourism. A $1.9 billion industry in the U.S., Tourism is another heavily impacted sector. Globally, tourism is a nearly $2 trillion industry. UN estimates predict that global tourism will be down by at least $1.2 trillion in 2020 and as high as $3.3 trillion (4.2% of global GDP) should the drop in tourism extend for 12 months.

Manufacturers serving these services industries are also impacted. Serving Tourism is Aircraft Manufacturing with annual revenues of $688 billion. With US airlines experiencing 90% revenue drops, Boeing has seen a 65% drop in revenue.

The tight linkage between Tourism and Aircraft Manufacturing is a single example of the myriad, complex interdependencies that make up modern economies. That fact supports caution when we consider the speed of recovery as well as the shape of the post COVID-19 world.

Based on recent economic history, we can be certain that a return to 2019-level activity across the entire economy is going to take many years. Consider the six years and more it took the U.S. economy to restore employment levels after the recession of 2008. Given the greater severity of the pandemic recession on many economies, the recovery period back to 2019 levels will be lengthy.

No Return to the Old Normal

For most, a full return to our prior patterns of living and working is the only desirable outcome. While much will be restored, a full return to the former status quo is not going to happen.

No one can predict precisely how long consumer consumption adaptation patterns to COVID-19 will endure. Some will have few options. Many Millenials, their earnings already hurt by the 2008 Great Recession and injured yet by another economic downturn, will curtail their spending yet again. Students from kindergarten to post-doc levels will be challenged by the pandemic’s impact on education. Schools and universities are already struggling to adapt to the current economic realities, never mind manage the health of their students and staff.

Besides economic disruption across the economy, other factors will influence the shape of the post-COVID payments industry.

The Digital Shift and Payment Industry Evolution

The pandemic’s impact will not be measured solely by how long it takes to return to 2019 levels of economic activity.

The pandemic will also be viewed as an historic forcing function across multiple aspects of life and work, specifically our expanded experience and reliance on digital technology.

Consider the impact of work-from-home orders on many in the services industries. The wide availability of broadband internet access via fixed and wireless connections, coupled with cloud-based delivery of services like Zoom and Slack, have enabled continued productivity by workers forced to remain home.

Glenbrook has spoken with multiple providers of services to billers and merchants who, for example, were able to disperse call center operations to their employees’ homes in a matter of a few weeks.

The impacts of this success, and the reduction or elimination of commuting time, are many:

- Transit system usage has dropped. Transport modality shifts have taken place, i.e. from subways to bus routes. Subway and train volumes are down 80%, stressing transit agency budgets.

- While vehicle miles traveled (VMT) have recovered in many areas, some areas continue to see reductions of 12% to 20%. As a result, fuel sales are down, cycling and scooter sales are up. As of mid-June, gasoline sales in the U.S. were down over 20% and are not expected to return to 2019 levels until 2023.

- Commercial real estate, particularly for operators of office parks and open concept workspaces, is facing new conditions as tenants reassess their space needs. Rents are down in San Francisco and New York.

- Sales and rental prices of suburban homes have increased as urban dwellers, fatigued by work-from-home orders and the loss of urban amenities, opt for more spacious dwellings

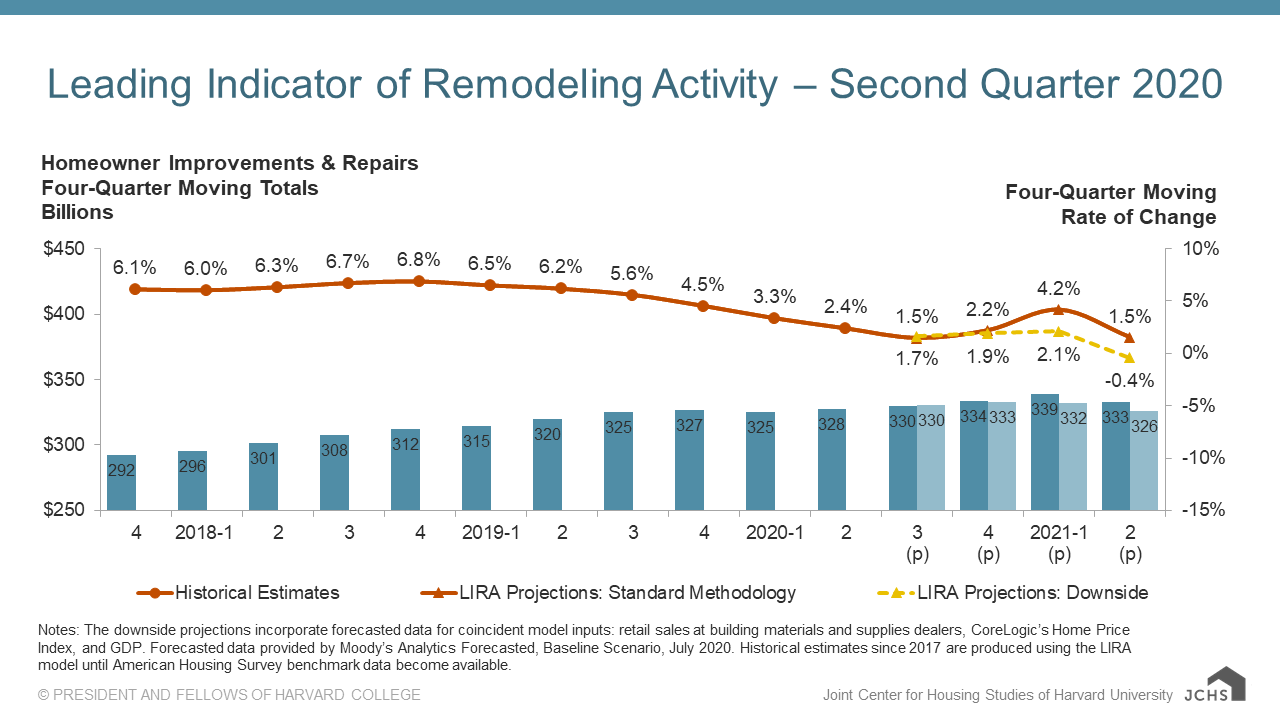

- While remodeling activity was bolstered by DIY projects during the first quarter (Home Depot’s foot traffic is up 35% YOY), other forecasts suggest concern over employment and general economic conditions will depress spending in 2021.

{kind=link}

The impact of these linked behavioral shifts on payment activity is obvious.

As individuals, most of us will return to a form of the old normal but not in every aspect of our lives. For others, without employment, healthcare coverage, and facing eviction, the results could be catastrophic.

For many businesses, even a 5% revenue decline can have a major impact on that enterprise’s stakeholders: employees, supply chain partners, stockholders, and customers. The impact of even modest changes in buyer behavior is consequential and often in unexpected ways.

Secular Trends Amplify the Digital Shift

The pandemic has forced individuals, families, government, and businesses to adapt. Those adaptations are facilitated and accelerated by secular changes that include:

Technology Enablement. As never before, we now have information technology tools enable remote work:

- Cloud computing has scaled to accommodate the shift to online work

- Broadband communications to the home and office provides the channel to exchange data at high speeds

- Web-based development delivers business and entertainment services to homes and offices, with data integration via APIs.

- Laptops, tablets, and smartphones are ubiquitous, mobile devices increasingly dominate usage, assuring access to cloud capabilities for many

- And when web-based tools are insufficient for a compelling user experience, downloadable software enhances the experience via apps

Demographic Readiness. As important as the tech, the global working population is largely comprised of digital natives, those who are entirely comfortable with digital tools for collaboration, service delivery, and, of course, entertainment.

Combined, these trends have enabled a critical mass of people to shift an even greater proportion of their lives to the digital realm. The extent of this shift would have been lower even five years ago.

While the extent of the shift will vary by activity, in Glenbrook’s view, much of this pandemic-pushed digital shift will be permanent. With a vaccine, sports, bars, restaurants, and live entertainment will return to pre-pandemic patterns and levels. Air travel, especially for business purposes, will not, given the success of virtual meeting technology. For many companies, work-from-home operation will assume a greater role, with concomitant impact on office space needs, employee transportation, and more.

Between Now and Vaccination

The bad news is that between now and widespread vaccination, economies at all levels will struggle with the management of COVID-19 as new outbreaks, and the resulting oscillations in social and economic activity, demand response. These will continue to depress payment activity in some domains, increase it in others, and complicate planning for everyone.

The steps taken to reduce COVID-19 infection rates are the same ones that keep them low. Planning for another 18-24 months before an effective vaccine becomes broadly availability seems prudent. Planning for further business disruption during this period is similarly prudent.

Permanent Swings in POS and Remote Commerce Domain

As our COIVD series has demonstrated, the pandemic is an accelerant to the ongoing trend toward end-to-end digital payments. For the card schemes, for example, this means payments are initiated without the use of a physical card to tap or dip at a physical point of sale.

The extent of this digital shift will vary by domain. The POS Domain is the biggest loser; Remote Commerce is the clear winner. Retail giant Walmart’s e-commerce business has nearly doubled from 2019. In response to pandemic, the company added delivery and pick up times. Given the convenience, never mind the safety, a portion of Walmart customers will choose those options on a more or less permanent basis.

POS Domain

The pandemic has had enormous negative impacts on restaurants, hospitality, and apparel, among many segments. Even with a vaccine, herd immunity, and robust restoration of economic activity, the pandemic will permanently alter demand and how services are brought to market.

Other trends in the POS domain include:

Touchless is the new POS buzzword. “Touchless” is the current term for how a growing number of consumers wants to pay. Few want to touch a payment terminal. Mastercard reported during its second quarter that contactless transactions were 37% of in-person transactions, up 9% over a year earlier. Credit union processor PSCU reported in August that debit transactions via mobile wallets were up 76.6% YoY with credit up 48.2%.

Unfortunately, contactless transactions at some merchants, even those initiated via Apple Pay or Google Pay, still require the consumer to select credit or debit because the merchant’s software has not been updated to read BIN ranges or take other measures to speed the checkout flow.

Expect to see more ISVs and PSPs update their software to eliminate the need for a consumer to ever touch a payment terminal.

QR Codes at the POS. QR codes are the principle payment initiation method in many markets, especially across Asia. Their use in payments in the U.S. has been muted with Starbucks and its simple 2D barcode as the earliest use case. Walmart has since deployed its app using QR codes. Using a linked card, the consumer starts the app and scans the barcode to initiate the transaction. Others have copied the merchant-specific app approach.

PayPal is using QR codes to re-enter the POS domain. At the end of July 2020, CVS and PayPal announced the ability to pay for CVS purchases using the PayPal or Venmo app. PayPal has partnered with InComm to take advantage of the connectivity that firm already has in place at many major retailers.

In all of these QR cases, the user experience is touchless. Expect to see providers of services to the tourism, hospitality, and restaurant sectors, already hurting from significant declines, to expand their use of touchless technology.

Remote Commerce Domain – The Shift is On

For most Americans and many around the globe, the pandemic has shifted a greater portion of their retail activity online to the Remote Commerce domain.

E-commerce in all its forms is the principle beneficiary of the pandemic-induced shift in consumer purchasing behavior. Amazon, of course, has benefited disproportionately from this sea change, reporting that its latest quarterly earnings bumped revenue 9.2% higher than Wall Street excepted.

Some portion of the COVID shift will be permanent, raising 2019’s 16% share of Retail volume even higher. In Q2, Mastercard reported that over 50% of its transaction were card not present. While unlikely to remain at that level, the number for 2020 will take a significant jump over 2019. Early surveys of holiday shopping plans show that most consumers, across all age groups, plan to make more than half of their purchases online this year.

As we have pointed out, even a 5% reduction in transaction volume will hurt multiple stakeholders. Small Main Street retailers and their mall-based competitors have all taken another blow. The biggest retailers like Walmart and Home Depot, better able to take advantage of the pandemic, are emerging as winners. While Target has tripled its online sales, commercial real estate firms with retail exposure and mall operators are experiencing pressure due to COVID-19, on top of what is a multi-year increase in consumer disenchantment with the mall and department store experience.

Subtler Shifts in Other Domains

The digital shift will continue to impact the other domains but in subtler ways:

Bill Pay Domain. Billers will pursue more opportunities to reduce paper and lockbox dependencies to speed collections, reconciliation, and improve cash flow.

B2B Domain. The advantages of straight through processing of invoices and receivables in B2B supply chains will encourage new data sharing methods if not the use of faster payment systems (businesses aren’t in a rush to pay).

P2P Domain. Consumer desire for touchless transactions as well as convenience is driving growth. Zelle volume is up 60% during the first half of 2020 versus the prior period. One third of small businesses are now able to accept Zelle payments.

Income Domain. Based on complications experienced during implementation of the CARES ACT, the Income domain may offer opportunity for both regulators and solution providers to simplify distribution of social benefits.

The Changed Competitive Landscape

Glenbrook concludes every Payments Boot Camp® with the Darwinian admonition that adaptability is essential to the long-term survival of both start-ups and industry incumbents. Conditions change even under normal circumstances. These anything-but-normal circumstances have exposed multiple frailties in some industries (restaurants, airlines) while amplifying the proposition of others (e-commerce, Amazon).

The payments industry has seen significant drops in volume before but nothing to this magnitude, despite, to this point, its short duration. Nor have we seen transaction reductions so prejudicial to some segments while so favorable to others. Some payment service providers with a hard focus on an affected sector, restaurants for example, are in survival mode. There is a growing tidal wave of business bankruptcies that will remove tens of thousands of merchant businesses from acquirer and processor roles.

For an industry tied to transaction volume, this is a gloomy prospect. The transaction pie has gotten smaller and even with economic recovery its shape will be different. Depending upon your role and company wherewithal, that 5% shift in business activity may be a minor irritant or an existential threat. But what about a months long 20% or even 40% drop? These unprecedented conditions will challenge business leaders responsible for navigating their enterprises through this period.

New technology tools, new methods of payment, and demographic preferences had already begun to alter the marketplace before COVID-19. Now, the pandemic is forcing payments industry participants to be nimble and adaptable to the new circumstances. These circumstances favor firms with current technology and the ability to quickly adjust business models.

Incumbents are confronted on the margins by the new competitors. But their own size and operational legacies constitute a larger barrier to their adaptation to new conditions. Further, in multiple markets around the world, regulators are either leveling the playing field or building new payment rails.

Even merchant-run payment services are gaining momentum. Taking advantage of the cloud, APIs, app stores, and smartphone ownership, Rappi Pay in Latin America and Oxxo Pay in Mexico are just two examples.

The payments industry is in an intense period of change, amplified and exacerbated by COVID-19. Beyond cost management, strategic options include new customer experiences, new front and back office capabilities, taking share from competitors, divesting business lines, the addition of new lines of business via merger, acquisition, or organic development. And more.

The status quo is gone. Glenbrook is ready to assist as you evaluate strategic options under these altered circumstances. Beyond short term adaptations, preparation for the post-pandemic era is a priority. Get in touch.

This series examines these impacts, and others, in more detail through Glenbrook’s Domains of Payments framework.

Please return to the series home page, to the Payments Views website, or sign up here to be alerted when the next installment is published.

[Domains]