Part 1 established the missing context layer and illustrated what the experience looks like across three purchase types. The key question is not whether agents with persistent context will exist, but how their role differs by category, where the technology is being built, and how far along it actually is.

Why Delegation Is Not Uniform

The industry has been discussing agentic commerce as a single phenomenon. In practice, the agent’s role varies along several dimensions:

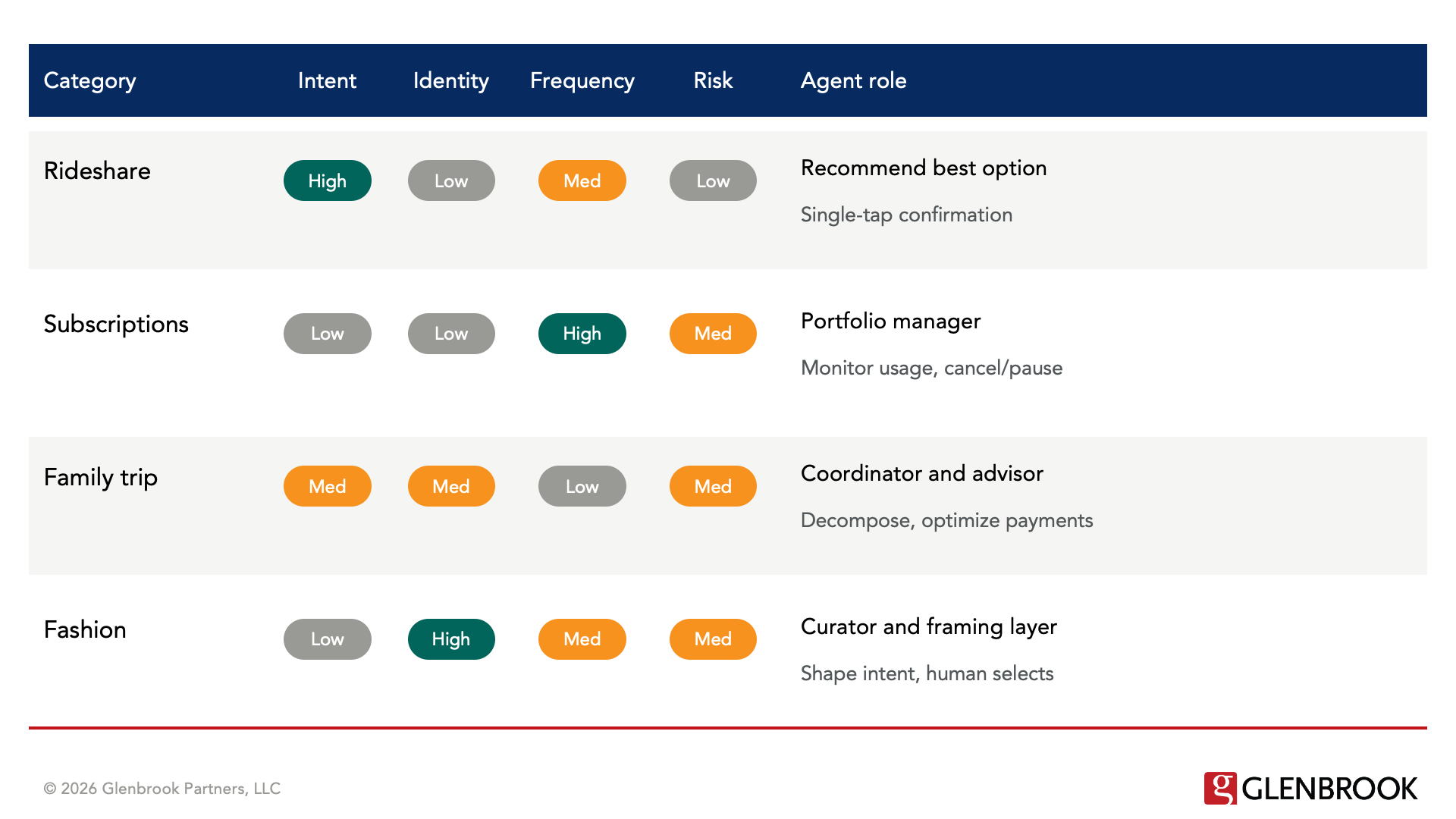

Intent clarity. When the consumer knows exactly what outcome is needed (a ride to a meeting), the agent can execute autonomously. When intent is vague or emerging (a dress for a trip the consumer has not fully planned), the agent curates and refines. The higher the intent clarity, the more the agent can do without human involvement.

Identity sensitivity. Some purchases express taste, self-image, status, or emotion. Others are primarily functional. A consumer who happily delegates rideshare selection may want full control over which dress she wears to dinner in Positano. The more a purchase reflects identity, the more the consumer will want to remain in the loop.

Frequency. Recurring interactions build a thicker base of behavioral data for the agent. Routine rideshare trips, subscription renewals, and repeated purchases in familiar categories give the agent more context to work with over time. Episodic or infrequent decisions (a family vacation, a major electronics purchase) require more active engagement because the agent has less prior behavior to draw on.

Risk and reversibility. Low-stakes, easily reversible purchases can tolerate more agent autonomy. High-stakes or difficult-to-reverse purchases (a contractor hire, a significant financial commitment) will require stronger human-in-the-loop confirmation.

Across categories, the agent performs a consistent set of functions: filtering what enters consideration, ranking what appears most relevant, framing trade-offs, timing when decisions are surfaced, and executing the chosen action. But the balance between agent authority and human judgment shifts depending on where a purchase falls along these dimensions.

Mapping Merchant Types Across Dimensions

Rideshare sits at one end: high intent clarity, low identity sensitivity, medium frequency, high delegation. The agent compresses the decision to a single confirmation. Fashion sits differently: low-to-medium intent clarity, high identity sensitivity, medium frequency. The agent curates and frames, but the human selects. Subscription management is a particularly interesting case: low active intent (many subscriptions persist through inertia), low identity sensitivity, high frequency. The OS-level agent has a unique advantage here because it can observe actual app usage across the consumer’s devices. It knows that Maggie has not opened a streaming service in three months, that she uses one news app daily but another only once a quarter, and that two of her subscriptions renewed last week at higher prices than the prior period. It can surface this information and suggest cancellations, pauses, or downgrades. The consumer still decides, but the agent makes the invisible visible.

This has a direct implication for merchants. Any company that sells across multiple categories or business lines will find that the agent interacts with each one differently. A hotel chain that also operates restaurants and a loyalty program faces three distinct agent relationships: the hotel booking is a compound-intent, mid-delegation interaction where the agent coordinates across travel sub-decisions; the restaurant reservation may be high-delegation and nearly automatic; the loyalty program becomes machine-readable data that the agent optimizes across competitors. Merchants need to evaluate each of their business lines against these dimensions and understand where they are exposed to agent-led selection, where they retain influence over the consumer’s decision, and where they need to build agent-accessible interfaces to participate at all.

China as the Observable Model

China provides the clearest early signal of how this develops because its ecosystem is structurally closer to the requirements of an OS-level agent layer.

Super-app ecosystems like WeChat already unify discovery, interaction, and payment within a single environment, so Chinese consumers are accustomed to commerce experiences where the platform manages most of the workflow. The step from that model to agent-mediated commerce is shorter than it would be in a market where consumers navigate between separate apps for each task. According to Poe Zhao’s reporting in the Interconnected newsletter, when OpenClaw launched, paid setup services appeared on Chinese consumer platforms within days, typically ranging from $7 to $40 for remote installation, and many of the people paying for installation had no specific use case in mind. The urgency was about not falling behind, not about a defined productivity goal.

The trajectory of agent adoption in China is instructive for anyone thinking about how this plays out for consumer commerce. Zhao’s reporting documented how different architectural approaches to the agent layer produced very different ecosystem responses. ByteDance’s Doubao Phone Assistant, which operated by reading screens and simulating taps across apps without their cooperation, was blocked by Tencent, Alibaba, and Meituan within days of launch. OpenClaw, which uses open protocols and keeps data local to the user’s device, was actively promoted by the same companies that blocked ByteDance.

The lesson is about control and incentive alignment, and it matters for the commerce discussion. An agent layer that positions one company as an intermediary between users and every app on their phone will be resisted by incumbents. An agent layer that generates revenue for everyone in the ecosystem will be embraced.

The more significant development, as Zhao noted, is the emergence of agents built directly into the phone’s operating system. Xiaomi, Huawei, and other Chinese device makers are developing and rolling out early system-level agent capabilities with native access to device context: messages, contacts, calendar, location, and connected devices. Unlike OpenClaw, which requires manual installation and configuration, these agents are designed to be present from the moment the phone is activated, accumulating context continuously without any action from the user.

For consumer commerce, this is the category that matters. An OS-level agent has persistent access to the full device context. It can shape how consumers discover, evaluate, and decide, not just how they transact. And it is controlled by the OS provider.

The U.S. Path

The U.S. does not have super-app ecosystems. Consumer behavior is organized around fragmented, single-purpose applications. Americans open one app to check the weather, another to hail a ride, another to order groceries, and another to browse clothing. The behavioral distance between this fragmented model and the kind of unified, system-mediated commerce experience that Chinese consumers already use is significant.

However, the U.S. has something that may matter more: two companies that control the dominant mobile operating systems. Apple and Google are the natural providers of an OS-level agent layer in Western markets. Apple has previewed an agent-capable Siri with personal context awareness and cross-app execution, built on its on-device Apple Intelligence infrastructure. Google is integrating Gemini into Android and actively building commerce-specific agent protocols. The detailed state of what these companies have shipped, what they have confirmed, and what remains to be built is assessed in the next section.

The value proposition of an OS-level agent may actually be stronger in a fragmented ecosystem than in a super-app environment. In China, WeChat already provides a degree of cross-service integration. In the U.S., the consumer bears the full cognitive burden of navigating between apps, comparing options across services, and managing context that does not transfer between applications. An OS-level agent that can operate across apps with a unified understanding of the consumer’s intent, preferences, and constraints addresses a pain point that is more acute in the U.S. than in China.

The question is whether Apple and Google will build these capabilities as open, interoperable layers or as proprietary extensions of their existing platform economics. Apple’s historical approach to platform features, tightly controlled, deeply integrated, and designed to reinforce ecosystem stickiness, suggests one answer. Google’s approach, more open but monetized through advertising and data, suggests another. Both paths lead to an OS-level agent. The governance model and the incentive structure behind that agent will differ.

The adoption curve will also differ. Chinese consumers moved rapidly because the behavioral shift from super-app-mediated commerce to agent-mediated commerce is relatively small. U.S. consumers will need to develop trust in a system that operates across their apps, accesses their financial data, and makes decisions on their behalf. The scenarios described in Part 1, a ride that books itself, a dress purchase shaped by calendar and financial context, a family trip decomposed into managed sub-decisions, represent where the technology is heading as the building blocks converge. Whether consumers adopt them will depend on the quality of the experience, the privacy safeguards in place, and the trust the agent earns over time.

The rideshare scenario is likely the earliest adoption point from the consumer’s perspective: high intent clarity, low identity sensitivity, and an interaction model that saves obvious time with minimal risk. If the agent gets the first few rides right, the consumer learns to trust it. That trust then extends into adjacent categories. The progression from high-delegation utility purchases to mid-delegation identity-sensitive purchases to compound-intent coordination will likely follow the consumer’s growing confidence in the agent’s judgment.

However, the categories where the agent delivers the best consumer experience are also the categories where merchants face the most pressure. When the agent recommends a rideshare provider based on availability, price, and reliability, the provider is reduced to a service layer competing on quantifiable metrics. The provider loses the in-app experience it has built to drive upselling, advertising, loyalty engagement, and habitual usage. Uber’s entire business model depends on consumers opening the Uber app, where Uber controls the experience, the default options, and the cross-sell opportunities. An OS-level agent that presents Uber as one option alongside Lyft and Waymo in a single notification strips all of that away.

The categories where consumers benefit most from agent mediation are the same categories where merchants have the strongest incentive to resist it, by limiting API access, restricting agent-readable data, or building proprietary agent experiences that keep the consumer inside the merchant’s own ecosystem.

This creates a predictable tension. The categories where consumers benefit most from agent mediation are the same categories where merchants have the strongest incentive to resist it, by limiting API access, restricting agent-readable data, or building proprietary agent experiences that keep the consumer inside the merchant’s own ecosystem. How this tension resolves, whether through consumer demand forcing merchant cooperation, regulatory pressure requiring interoperability, or OS providers leveraging their platform position to compel access, will shape the pace and pattern of adoption.

Where the Technology Stands Today

The scenarios in Part 1 are forward-looking. Being precise about what exists today versus what is projected matters, because the gap determines the timeline the industry should be planning against.

The foundational infrastructure is real and shipping. Apple Intelligence provides on-device processing, a privacy architecture (on-device Neural Engine plus Private Cloud Compute for complex tasks), and a developer framework for third-party integration on supported devices within Apple’s global ecosystem. Google’s Gemini is integrated into Android and is being incorporated into AI-driven shopping experiences in Search. In China, Xiaomi, Huawei, and others are developing and rolling out early system-level agent capabilities with native device access, and OpenClaw has seen visible early adoption and significant ecosystem response. The transaction protocols (Visa TAP, Mastercard Verifiable Intent, UCP, AP2, A2A) are live, though real-world agent-mediated transaction volume remains minimal.

The critical next capabilities have been announced but have not shipped. Apple has said it is working on a more personalized Siri with awareness of personal context and the ability to take actions within and across apps, but acknowledged the rollout has slipped. More specific 2026 timing has been reported but remains fluid. In January 2026, Apple and Google entered a reported multi-year deal to power the rebuilt Siri with Gemini models; Bloomberg separately reported the cost could be approximately $1 billion annually. Apple’s track record on this specific set of capabilities includes multiple delays, and the company pulled advertisements promoting features that had not yet shipped.

The persistent preference model that the Maggie scenarios describe does not exist in production anywhere. Apple’s personal context features, when they ship, will let Siri find a specific piece of information on your device (a passport number in an email, a flight confirmation in a message). That is meaningfully different from an agent that has learned over months that you prefer warm earth tones, typically spend $120 on a dress, and buy travel clothing four weeks before a trip. Building that persistent model raises significant privacy questions: where is it stored, who trains it, and what are the tradeoffs between on-device sophistication and cloud-based capability?

These are solvable problems, not fundamental barriers. The trajectory is clear and the investment levels from Apple, Google, Xiaomi, Huawei, and Meta strongly suggest that these companies view this as central to their strategies. The question for the payments industry is not whether this arrives, but how quickly.

In Part 3, we explore the specific implications for the payments and commerce industry: how discovery changes when agents mediate it, how payment selection shifts upstream, how merchants need to prepare differently across categories, and who ultimately controls the agent layer.