Parts 1 and 2 established the context layer and how agent behavior varies by category. The question now is what breaks.

What This Means for the Industry

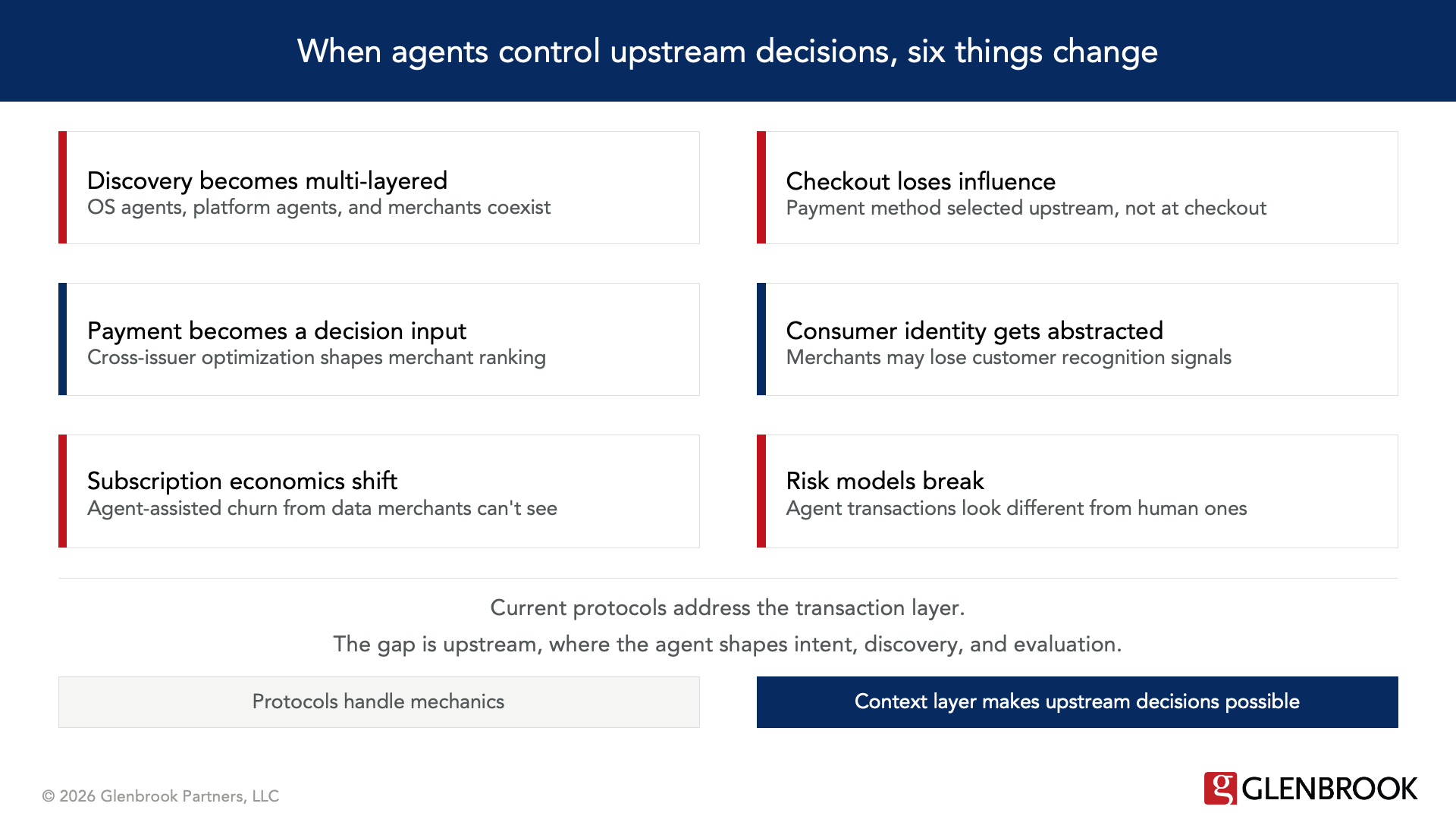

The current wave of agentic commerce protocols is built to address the transaction layer, and those protocols represent genuine progress. The gap is upstream. When an agent shapes the consumer’s intent, discovery, and evaluation before any transaction begins, several assumptions embedded in the current infrastructure come under pressure.

Discovery becomes multi-layered.

The agent does not replace search, social, and advertising. It sits on top of them. Meta has signaled that it is developing AI shopping tools across Instagram, Facebook, and WhatsApp designed to interpret intent and compare products across merchant catalogs. Google is integrating agent-driven shopping into Search. Both companies are investing tens of billions in AI infrastructure to support this direction.

The OS-level agent adds another layer above these platform-specific agents. It operates across all of them with a unified view of the consumer that no individual platform possesses. Meta knows what Maggie engages with on Instagram. Google knows what she searches for. The OS-level agent knows both, plus her calendar, financial accounts, messages, and purchase history across every merchant and platform. Merchants that lack structured, machine-readable data (inventory, sizing, shipping speed, return policies, pricing) risk exclusion from agent-driven consideration sets regardless of which layer is doing the filtering.

Whether these agent layers will cooperate is an open question. Google’s A2A protocol provides the technical basis for inter-agent communication, but the incentive alignment is unclear. Meta’s commercial model depends on keeping consumers inside Meta’s surfaces. If Meta’s agent hands off to an OS-level agent that compares its recommendation against competing platforms, Meta loses control of the outcome. Whether these layers cooperate or compete will significantly shape the consumer experience. Open banking frameworks are also relevant here: the agent’s ability to do cross-issuer payment optimization depends on permissioned access to the consumer’s financial data across institutions, an area where the U.S. is still early despite progress on the CFPB’s Section 1033 rule.

The checkout flow loses influence.

Every lever a merchant currently uses to steer payment selection at checkout, the order methods appear, default selections, BNPL presentation, friction on certain options, weakens when the agent has already recommended or selected the payment method upstream. The merchant receives a transaction with a payment method already chosen based on the consumer’s full financial context across all their accounts. This has implications for interchange revenue expectations, BNPL attach rates, and the economics of payment method steering.

Payment moves from execution to decision input.

In the Maggie scenario, the agent surfaced an Amex statement credit and a Chase Sapphire points multiplier as part of the purchase decision, not at checkout. That kind of cross-issuer, cross-instrument optimization is something no single bank app, merchant checkout, or payment processor does today. An agent with access to the consumer’s full financial context across accounts can do it, and the OS level has the most direct path to that access because all the financial apps live on the same device. Open banking frameworks could enable similar access for third-party agents, but the infrastructure for real-time, agent-accessible financial data across issuers is still early. Merchants that expose payment incentives in machine-readable form (statement credits, category multipliers, promotional financing) create opportunities for the agent to factor those into merchant ranking. Merchants that do not expose this data may find that the agent optimizes around them.

Consumer identity may be abstracted away from the merchant.

If the agent presents a token or virtual card rather than the consumer’s stored credentials, the merchant loses the ability to connect the transaction to a customer profile. Loyalty, CRM, personalization, and repeat-purchase economics all depend on that connection. Visa’s TAP is designed to enable agents to pass consumer identifiers (token IDs, loyalty accounts, device identifiers) to help merchants recognize returning customers. Whether the agent shares these identifiers, and under what conditions, becomes a control point.

Subscription economics face agent-assisted churn.

Visa’s Enhanced Subscription Manager and Mastercard’s Smart Subscriptions already give consumers tools to manage recurring payments through their banking apps. An OS-level agent takes this further. It can observe cross-service usage patterns, compare subscription costs against actual engagement, and proactively recommend cancellations, pauses, or downgrades. For subscription merchants, this is churn driven by data the merchant cannot see, initiated through a channel the merchant does not control. The productive response is to build agent-accessible interfaces that allow merchant-side agents to engage with the consumer’s agent and offer retention alternatives before a cancellation is executed.

Risk models will break.

Current fraud and risk models are built around patterns of human-initiated transactions. Agent-mediated transactions will look different: potentially higher velocity, different browsing patterns, different session characteristics. Risk providers will need to distinguish between legitimate agent-mediated commerce and fraudulent automation. The protocols provide some foundation (Visa TAP’s agent identity verification, Mastercard’s agent registration), but the models themselves will need to adapt.

The Control Question

The OS-level agent thesis raises a question about platform power that the industry needs to address directly.

When the agent lives on the device and accumulates a persistent understanding of the consumer over time, the agent’s memory becomes a new form of lock-in. Today, switching from iPhone to Android means losing some app configurations and ecosystem integrations. In an OS-level agent world, switching means losing the accumulated preference model that makes the agent useful: the sizing history, the taste profile, the financial patterns, the supplier preferences, the delegation rules the consumer has established over months or years. That is a switching cost that exceeds anything in the current mobile platform competition.

Apple or Google controlling the agent layer at the device level means controlling intent formation, preference learning, discovery, and the decision surface. The question of who controls the agent layer, who sets the ranking logic, who decides what data the agent shares with merchants and payment providers, and who owns the learned consumer profile will shape the next phase of platform power in commerce.

Data portability frameworks that exist today were not designed for the kind of accumulated, cross-domain behavioral model that an OS-level agent builds. Whether those frameworks extend to agent memory, and whether exported data is useful without the agent’s interpretive layer, is an open question with significant regulatory and competitive implications.

For the payments industry specifically, the relationship between the OS-level agent and the payment credential introduces new dynamics. If the agent controls which payment method is selected and how the consumer’s identity is presented to the merchant, the agent becomes an intermediary in a value chain that has historically connected consumer, issuer, network, acquirer, and merchant in well-defined roles. How the agent interacts with that value chain, and whether it operates within the existing structure or begins to disintermediate parts of it, will depend on the choices made by OS providers, networks, issuers, and regulators over the next several years.

The questions that matter are: who controls the agent, what context it has access to, how merchants and payment providers participate when the commercially significant decisions happen upstream, and whether the industry is prepared for a consumer experience that begins well before any transaction protocol is invoked.

Conclusion

Neither the transaction protocols nor the context layer alone gets us to the agentic commerce experience the industry has been describing. The protocols handle mechanics. The context layer makes upstream decisions possible. Their convergence is what advances the journey, and each layer is progressing on its own track.

Significant gaps remain. The persistent preference model that would allow an agent to learn a consumer’s taste, body, and financial patterns over months does not exist in production. The privacy architecture for that kind of accumulated model is still being designed. Inter-agent cooperation is technically possible but commercially uncertain. Merchant readiness is early. These are solvable problems, but they are not solved yet.

Consumers are already partway there behaviorally. They are using conversational AI for the upstream commerce activities described in this series: planning trips, comparing options, discovering products, forming intent through iterative conversation. What they are not yet doing is connecting that upstream activity to downstream execution. The context layer narrows that gap because the agent already has the consumer’s preferences, constraints, and history. The transition from discovery to action becomes smaller when the agent does not start from a blank prompt.

The questions that matter are: who controls the agent, what context it has access to, how merchants and payment providers participate when the commercially significant decisions happen upstream, and whether the industry is prepared for a consumer experience that begins well before any transaction protocol is invoked.

Those questions deserve attention now. The technology is advancing faster than most industry participants expect, and the time to prepare is before the capabilities converge, not after.